The White House released a healthcare reform framework in January 2026 that, if enacted, would expand transparency requirements for both insurers and providers — with direct implications for employer-sponsored plans.

Section 1: What the Plan Proposes

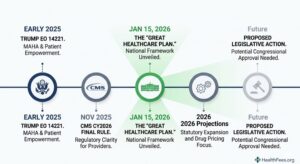

The US administration announced the “Great Healthcare Plan” on January 15, 2026, outlining a framework for healthcare reform focused on cost containment, consumer choice, and transparency. The proposal builds on prior regulatory initiatives addressing hospital and insurer price transparency, prescription drug pricing, and health plan disclosures, but contemplates broader statutory changes that would require congressional approval.

A significant focus of the plan is expanded transparency for insurers and healthcare providers, including eliminating certain payments to brokers and intermediaries and increasing insurer accountability, which may influence how insurers structure premiums and administrative fees for employer-sponsored plans.

Section 2: What It Means for Employer Plans Specifically

While the Great Healthcare Plan is a proposal rather than enacted law, employers sponsoring health and welfare plans should consider several strategic implications: changes to drug pricing and insurer transparency could affect overall plan expenses and future premium negotiations; employers may need to reassess arrangements with insurers, PBMs, brokers, and other service providers if pricing structures or disclosure obligations change; and expanded transparency and “plain English” standards could require updates to plan documentation and participant communications if such requirements are extended to employer-sponsored plans.

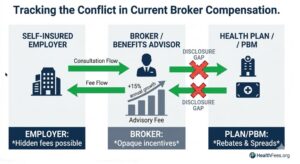

Section 3: The Broker Compensation Disclosure Question

One of the more consequential proposals: eliminating or restricting certain broker and intermediary payments.

If enacted, this would require employers to understand — and in some cases renegotiate — how their benefits advisors are compensated. Compensation structures that create conflicts of interest between advisors and plan participants have been a longstanding compliance concern under ERISA fiduciary standards.

Section 4: The Prescription Drug Transparency Angle

Lower drug acquisition costs may translate into reduced plan spending over time; however, changes to pricing models could also affect formulary design, pharmacy benefit manager arrangements, and global supply considerations for drug manufacturers.

In 2024, nearly a quarter of all employer healthcare spend went to pharmacy. Employers are forecasting an 11–12% pharmacy cost increase heading into 2026 — a situation not remediable by plan design changes alone, requiring exploration of non-traditional PBM models with increased transparency and reduced reliance on rebates.

Drug pricing transparency is the next regulatory frontier — and employers with high pharmacy spend are most exposed to how it resolves.

Section 5: What Employers Should Monitor and Do Now

CMS recommends that employers: engage service providers about implications for pricing practices and transparency requirements; review plan documentation and communications to evaluate whether they would be adaptable to potential plain-language or enhanced transparency standards; assess cost and fee structures considering potential changes to prescription drug pricing and intermediary compensation; and document fiduciary decision-making to ensure discussions and evaluations are appropriately recorded as part of governance processes.

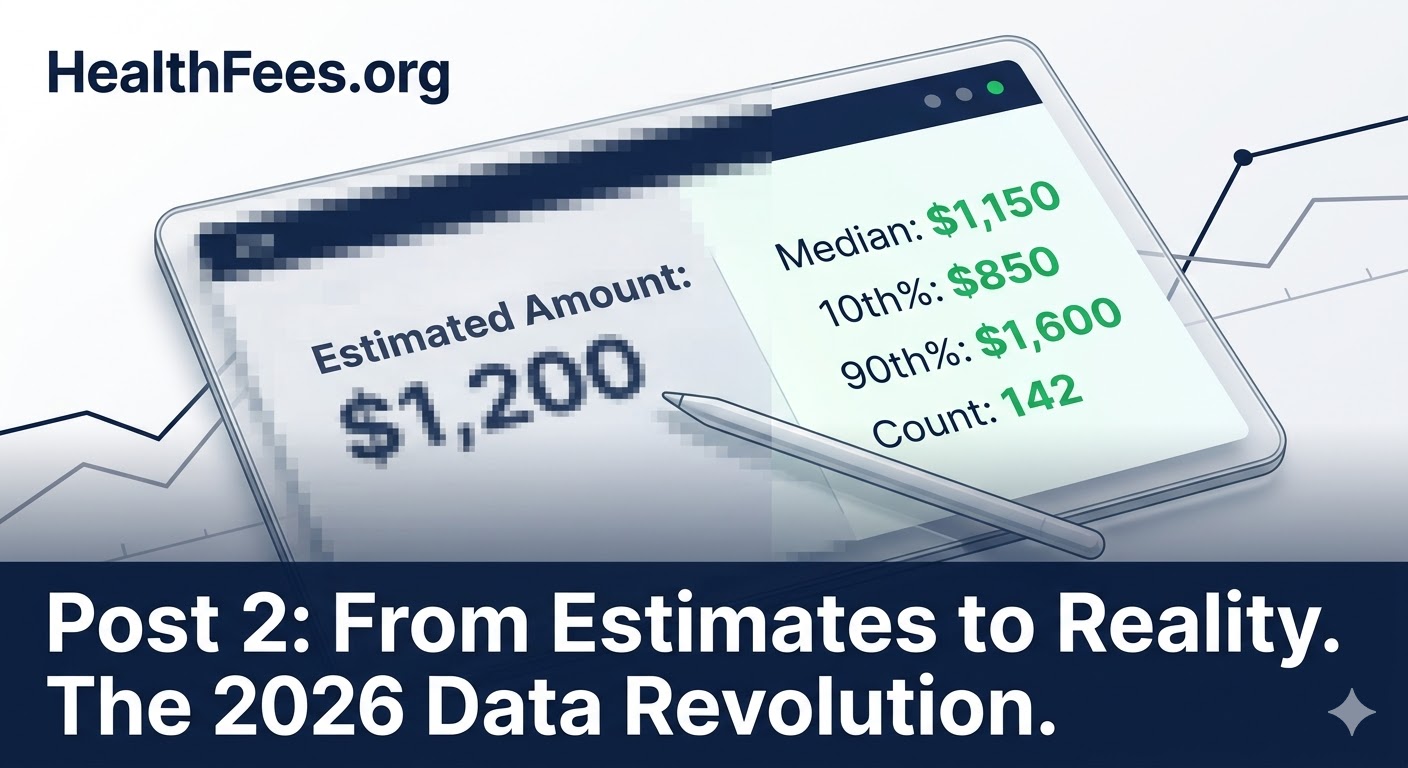

Use HealthFees.org to establish a baseline of what procedures cost in your market — a defensible reference point for plan governance decisions.