The federally mandated disclosure of millions of in-network negotiated rates has provided the first investigative look into the proprietary contracts that govern healthcare pricing in the United States. While proponents argued that this transparency would universally lower costs, early evidence suggests the impact is more nuanced: price reductions are occurring for “shoppable” services in competitive markets, but the market’s overall equilibrium is also being tested by providers who are now aware they have been systematically underpricing their services [as noted in a National Bureau of Economic Research study]. For the data to deliver its full potential, systemic issues with compliance and the usability of TiC machine-readable files (MRFs) must be resolved.

Scale of Price Failure Revealed by Negotiated Rates

The scale of price variation documented across the newly disclosed data sets confirms long-suspected market dysfunction. A cross-sectional study of commercial prices negotiated by five national insurers found massive price gaps within the same hospitals for the same services [detailed in a study published by PMC]. For inpatient services, the gap between the lowest and highest negotiated prices was, on average, a striking 86% of the Medicare rate. For outpatient services, this minimum-to-maximum gap swelled to 222% of the Medicare rate [reported by PMC researchers]. This data not only proves the existence of price steering but also suggests that up to 29% in potential savings could be realized if payers consistently targeted the minimum within-hospital negotiated price.

Measurable Price Convergence in Targeted Markets

Where transparency has been implemented and enforced, there is documented evidence of competitive pressure leading to price reductions. Analysis of state-level price transparency efforts, for example, found that the prices for certain elective, shoppable services decreased by an average of about 7.3 percent, or over $3,100, where data was readily available [according to research cited by the Healthcare Value Hub]. This drop was concentrated among high-priced providers who were compelled to adjust their rates to avoid being outliers. Conversely, some studies have noted a counterintuitive effect: when price information is made public, low-priced providers, realizing they were under-compensated relative to their peers, slightly increased their prices to match the market rate, leading to a marginal increase in overall billed charges in those specific segments [as documented by the NBER].

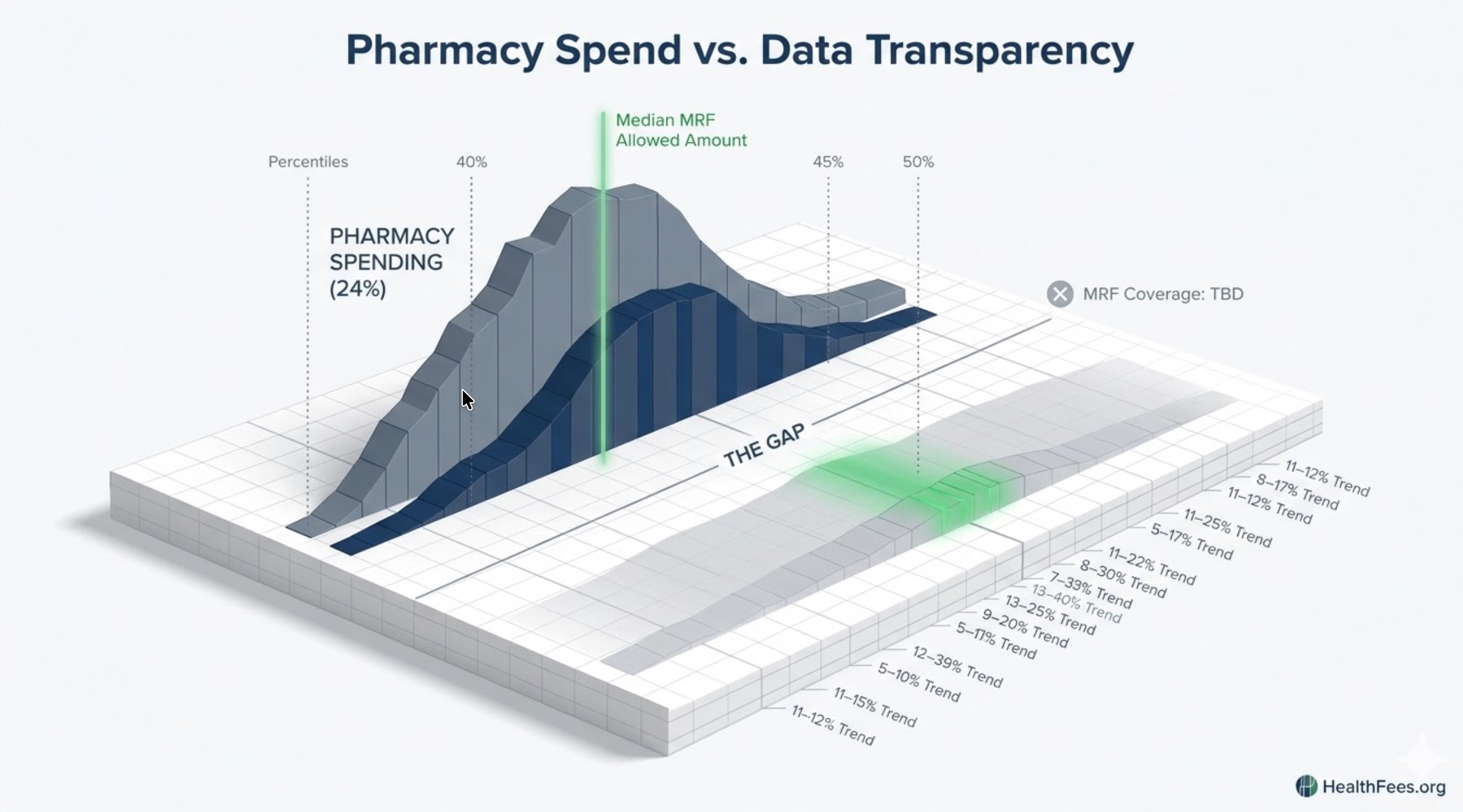

The Impediment of Compliance and Data Usability

The transformative effect of the data is being slowed by two key systemic obstacles: compliance failure and data complexity. A November 2024 investigative report found that only 21.1% of hospitals were in full compliance with all federal price transparency rules, a significant backslide from prior assessments [according to Patient Rights Advocate data]. Furthermore, the Government Accountability Office (GAO) has highlighted that the complexity and inconsistent format of the TiC machine-readable files (MRFs) posted by hospitals and payers impede large-scale research and systematic data use by purchasers [as noted in the October 2024 GAO report]. Until the enforcement is rigorous enough to yield complete, standardized data, the pressure on pricing remains localized and difficult to leverage widely.

The central implication of the transparency mandates is that the information asymmetry that long shielded providers and payers is ending. The massive price variations revealed by the in-network negotiated rates provide a clear and actionable benchmark for purchasers. While the No Surprises Act addresses the worst financial impacts of surprise billing for consumers, the core goal of systemic cost reduction hinges on whether regulators and the industry can overcome the current hurdles of incomplete data submission to allow true competitive market dynamics to take hold.