For the same major procedure, UnitedHealthcare’s negotiated rate at one Pennsylvania hospital was $18,066. At another Pennsylvania hospital, it was $87,457 — a 4.8x difference. Same insurer. Same state.

Section 1: The Data Behind the Variation

Even within the same state, the ratio of the highest to lowest negotiated rate averages 3.2 to 3.4 for major procedures. In Pennsylvania, the UnitedHealthcare rate for a major bowel procedure ranged from $18,066 to $87,457 at different hospitals — a ratio of 4.8.

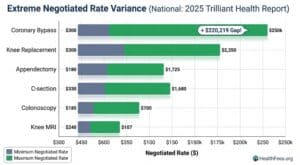

Procedures like coronary bypass ranged from $27,683 to $247,902 nationally — an absolute difference of $220,219.

These are not chargemaster rates — the inflated list prices hospitals publish and rarely collect. These are negotiated rates: what an insurer has contractually agreed to pay.

Section 2: Price Variation Does Not Track Quality

The intuitive explanation for wide price variation is that more expensive hospitals deliver better care. The data does not support this.

Within a sample of hospitals that have been featured on various “best hospital” lists, there was no observable correlation between aggregate measures of cost and quality.

Across six inpatient procedures, the average price difference between Aetna and UHC negotiated rates at the same hospital was $15,366 — for the same procedure, same facility, different payer.

If quality explained the price, you’d expect the same hospital to cost roughly the same regardless of insurer. That’s not what the data shows.

Section 3: What Drives the Variation

Very little variation in hospital prices is explained by each hospital’s share of patients covered by Medicare or Medicaid. A larger portion of price variation is explained by hospital market power.

Market power — the degree to which a hospital system dominates a regional market and can resist insurer pressure — is the primary predictor of high negotiated rates. It is not quality. It is not efficiency. It is leverage.

Section 4: The Geographic Arbitrage That Already Exists

In the Oakland, CA region, MRI claims were priced between $475 and $1,100 — with the average approximately 144% higher than in the Orlando, FL region.

Across five outpatient surgeries examined, the national median ambulatory surgery center rate was always lower than the median rate for hospital outpatient departments. For a colonoscopy, the median ASC rate was $2,454 — or 67.5% — less than the hospital rate, translating to aggregate potential savings of $4.5 billion annually for this single procedure alone.

The variation is not random. Site of care and geography are predictable variables — which means they’re actionable.

Section 5: How to Use This Information

For patients:

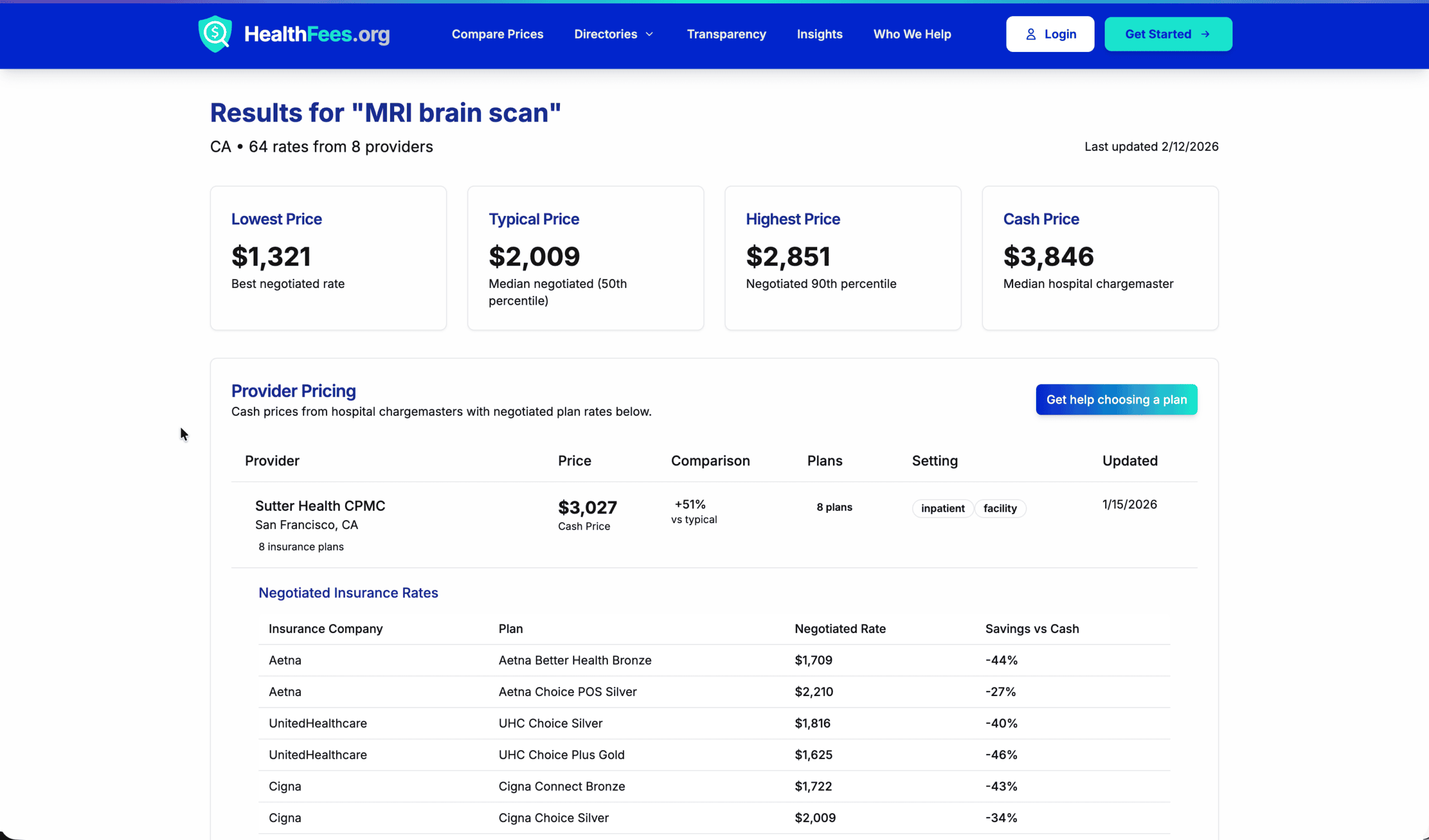

- For elective or shoppable procedures, comparing prices before scheduling is practical and consequential — a $3,000 vs. $9,000 MRI at two in-network facilities is a real difference in out-of-pocket exposure

- Ambulatory surgery centers often provide the same service at materially lower cost than hospital outpatient departments

For employers:

- Site-of-care incentive design — steering employees toward lower-cost facilities for appropriate procedures — is one of the highest-ROI benefit design levers available

- This requires knowing what the price spread actually is, which requires MRF data

Search your procedure at HealthFees.org. Compare what hospitals in your area actually charge — the variation may be larger than you expect.