In 2024, one in four employer healthcare dollars went to pharmacy. Hospital and physician price transparency rules now cover most clinical spending — but pharmacy remains largely outside the transparency framework.

Section 1: The Numbers

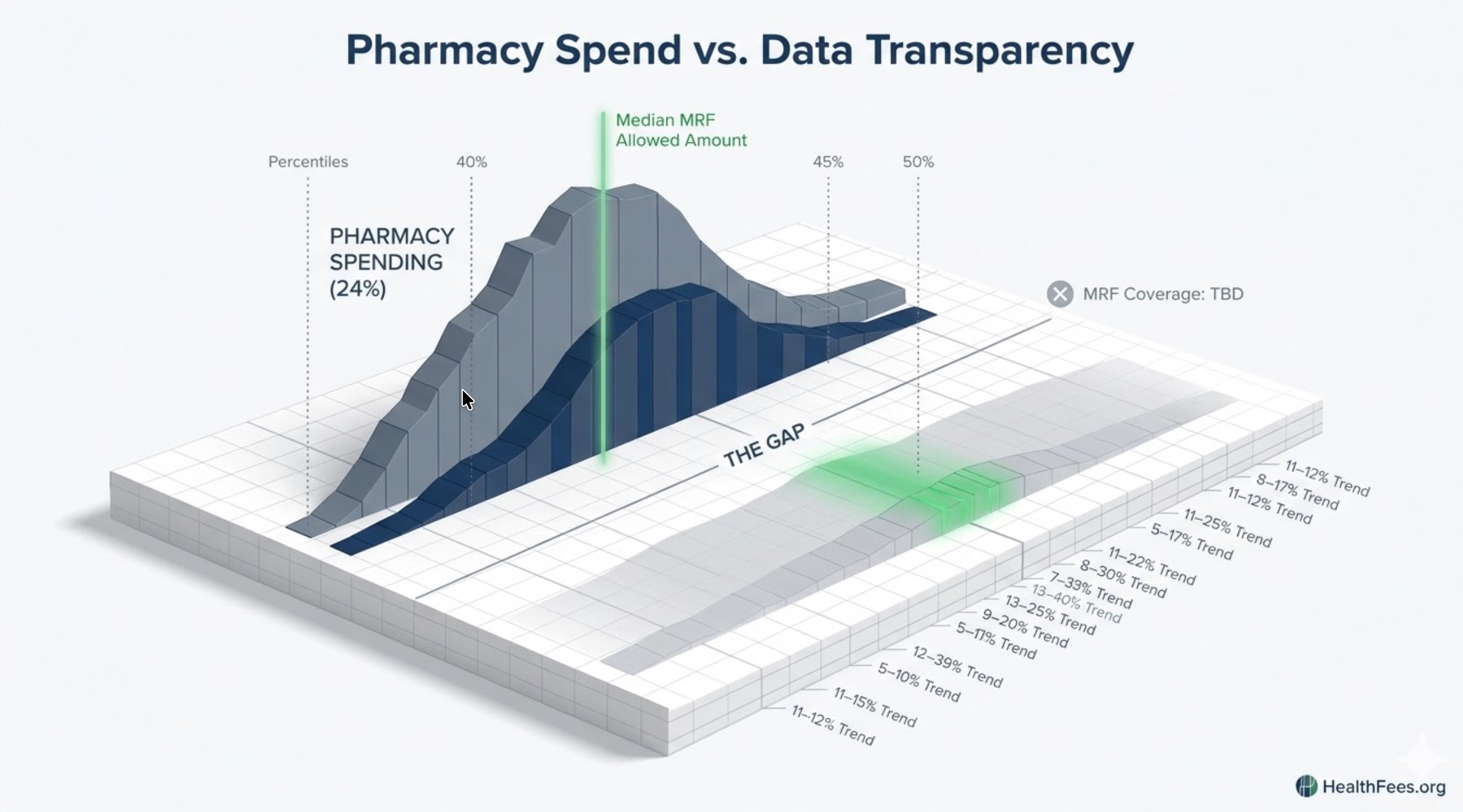

In 2024, nearly a quarter of all employer healthcare spend (24%) went to pharmacy expenses. Employers are forecasting an 11–12% increase in pharmacy costs heading into 2026. This cannot be remedied by plan design changes — employers need to explore PBM models that champion transparency and reduce reliance on rebates.

Pharmacy cost trend in 2026 is running 2.5 percentage points higher than the overall medical trend, reinforcing the urgency of managing pharmaceutical costs separately from medical spend.

Section 2: What Transparency Rules Cover — And What They Don’t

Current transparency architecture:

- Hospital MRFs (45 CFR Part 180): Cover inpatient and outpatient hospital services, including hospital-administered drugs billed as part of a procedure

- Transparency in Coverage Rule: Covers health plan negotiated rates for most medical services

- Pharmacy MRFs: The compliance requirements for prescription drug machine-readable files began in 2021, but federal agencies delayed the effective date until further notice. The agencies recently issued FAQs rescinding the prior enforcement delay, but the effective date for compliance is still “TBD” and pending future guidance.

The gap is significant: pharmacy — the fastest-growing cost category — has been the most delayed in transparency implementation.

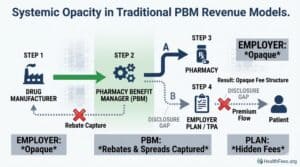

Section 3: The PBM Structure and Why It Creates Opacity

Pharmacy benefit managers sit between drug manufacturers, pharmacies, and employers. Their revenue model — historically built on rebates, spread pricing, and administrative fees — is specifically designed to separate visible costs from actual economics.

Employers must immediately explore implementation of non-traditional PBM models offered by incumbents and innovators alike, which focus on increased transparency and reduced reliance on rebates. Further, systemic change — whether brought on by dramatic marketplace moves or via government intervention — is necessary to bring down pharmacy costs for employers and employees alike.

Section 4: GLP-1s and the Next Escalation

GLP-1 utilization increased 744.6% between 2018 and 2023, while bariatric surgery volumes remained flat or declined — illustrating how medications are disrupting procedure-based care.

Employers are deciding if and how they should cover GLP-1 medications used to treat diabetes, weight loss, and other conditions. The cost burden led some employers to drop coverage for weight loss in 2026, though costs may be mitigated by a growing direct-to-consumer market, new oral formulations, and virtual solutions to manage costs.

GLP-1s are not a temporary spike. They represent a structural shift in how a major disease category is treated — and they are arriving before the transparency framework is in place to benchmark their cost.

Section 5: Where Regulation Is Heading

The Great Healthcare Plan proposes changes to how prescription drug pricing is structured, with lower drug acquisition costs potentially translating into reduced plan spending over time — though changes to pricing models could also affect formulary design and PBM arrangements.

A Drug Transparency Request for Information was issued in May 2025, requesting input on prescription drug MRF disclosure requirements — which may prompt future regulatory expansion of transparency rules into the pharmaceutical sector.

The trajectory is clear: pharmacy transparency is coming. The timing and form are still in development.

Start with hospital and medical pricing for your most common procedures at HealthFees.org. Understanding the baseline matters before the next cost category comes into view.